Stop Letting Response Rates Drive Strategy in Insurance Lead Generation

How KPI-driven outcome testing shapes profitable growth.

Insurance lead generation has no shortage of testing. The challenge is not whether teams test. The challenge is deciding what we are trying to learn before choosing how to test it.

Some programs begin with tools such as multivariate testing. Stronger programs begin with a KPI. They define the learning objective first, then select the testing method that best matches it. That distinction sounds small, yet it separates incremental optimization from breakthroughs that reshape a business.

The first two posts in this series examined how MVT often drifts toward creative refinement and why response rates alone cannot guide mailing frequency or capital allocation. This article moves forward on that foundation. The goal is not to replace MVT. The goal is to place testing methods inside a hierarchy driven by allowable CPS and profitable revenue.

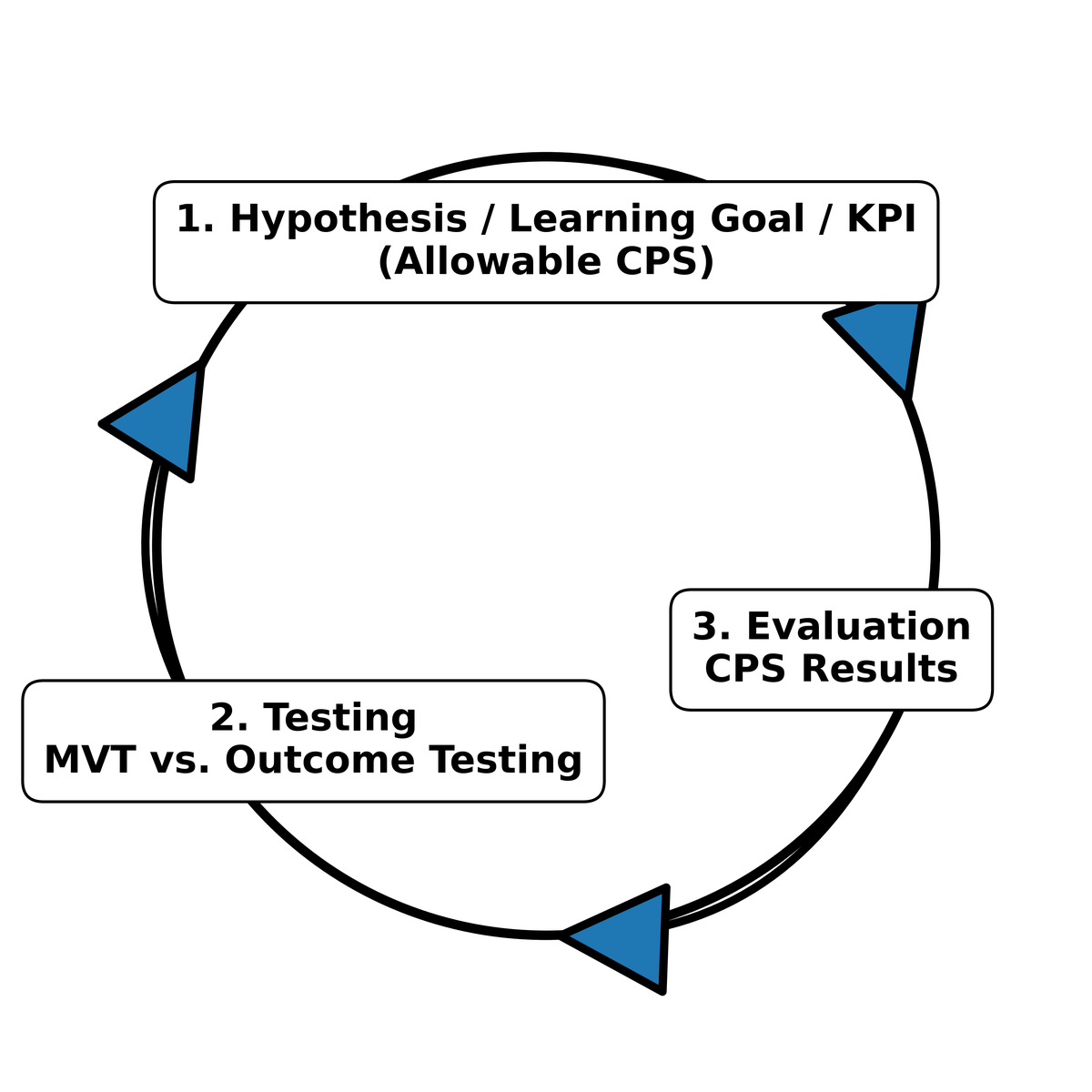

The Hierarchy That Should Guide Testing Decisions

Testing methodology should never come first. The hierarchy starts higher.

Level 1. Hypothesis, Learning Goal, and KPI

Every testing decision begins with the evaluation criteria. For direct response insurance programs, that usually means allowable CPS. The KPI defines what success looks like and shapes the question we are trying to answer.

Level 2. Learning Method

Once the KPI is clear, marketers choose the testing structure that fits the learning goal. MVT works well when refinement is needed. Outcome testing becomes more appropriate when leaders want to know whether an entire communication system should replace the current control.

Level 3. Evaluation Loop

Testing begins with the KPI and ends with the KPI. Response rates, creative metrics, and analytical models support evaluation, but profitable revenue remains the endpoint.

In practice, this is less a ladder with three steps than a circle. The KPI starts the process and closes the loop. Once the allowable CPS and universe size are known, leaders can quickly calculate the number of customers needed to achieve sales goals. If that number pushes penetration levels beyond available capital or manageable scale, the responsible marketer must tell decision makers that the goal is not achievable under current conditions.

Strategy is not linear. The KPI defines the question, guides testing decisions, and ultimately determines whether a system earns the right to scale.

Choosing the Method Based on the Learning Objective

Multivariate testing can perform full-format testing. Some insurance lead generators use it successfully that way. Yet in many real-world environments, MVT drifts toward element-level refinement because it aligns with existing production workflows and reporting structures.

Typical MVT activity includes headline variations, offer language tweaks, layout adjustments, guarantee phrasing, and incremental creative changes. These refinements can improve efficiency. They rarely change positioning or production structure. Outcome testing shifts the focus. Instead of asking which element performs best, it evaluates whether a complete challenger system displaces the existing control economically.

The Components of System-Level Testing

When outcome testing is used, the entire communication system is evaluated together: outer envelope, format, tone, positioning, offer structure, inserts, brochures, cards, and other contents, and personalization. Minor CPS improvements can displace a control gradually over one or two years. Larger structural wins are rarer. When a challenger produces roughly twenty percent or greater CPS improvement, many direct response teams consider it a super control. Super controls can last a decade or longer because they represent a structural advantage rather than a creative tweak.

A Breakthrough Example: Veterans Life Insurance

At Veterans Life Insurance Company, a traditional plastic card package served as the established control. A full challenger package was introduced using a facts-driven Snap Pac structure aligned with how veterans and civil servants expect information to be presented.

The result: production cost dropped by roughly twenty-five percent at rollout. Response increased by about twenty percent. The control was displaced. Production capabilities expanded to handle scale. The authority-aligned structure migrated into television and freestanding newspaper inserts. Affinity programs expanded across credit union affiliations, credit card memberships, and other membership-based audiences.

Institutional Tone and Long-Lasting Controls

A later example involving AARP membership mailings reinforced the same pattern in a different context. A Snap Pac challenger built around institutional tone and structural clarity replaced an existing control with lower cost and stronger response. The improvement qualified as a super control and held its position for more than ten years despite ongoing testing pressure.

Outcome Testing in Insurance Lead Generation

Outcome testing has also shaped insurance lead programs, such as work done for Blue Cross Blue Shield of Texas. Structural challengers displaced a primary B2C group health lead generation control and created new controls for segmentation groups, including students and associations. Response rates still played a role in evaluation. Yet CPS performance determined whether a challenger scaled.

Why Production Stability Sometimes Slows Innovation

Large breakthroughs often require operational change. Continuous MVT cycles feel safer. They maintain predictable workflows and reduce operational friction. Yet excessive stability can limit growth. When a challenger produces a structural CPS advantage, production must evolve to support it.

Analytics in the Right Role

Modern analytics platforms help confirm test integrity, validate tracking accuracy, and monitor performance during rollout. What they cannot do with certainty is predict how a fully integrated control package will perform until it is tested in the real world.

Super Controls and the Economics of Scale

A structural CPS reduction of twenty percent or more changes planning assumptions immediately. When a super control emerges, it influences frequency decisions, channel allocation, production investment, and long-term growth strategy.

A Practical Shift for Insurance Leaders

A practical shift for insurance leaders is not to abandon MVT, but to apply it with discipline and intent. MVT belongs inside a proven system where the objective is refinement and incremental improvement; outcome testing belongs where structural change is required, and real growth is at stake. The KPI circle is not a planning checklist — it is a decision discipline that keeps testing anchored to allowable CPS and forces strategy to align with economic reality. Both methods must be judged through allowable CPS, not response lift alone, and leaders must be prepared to make operational changes when a challenger demonstrates a genuine economic advantage. The KPI defines the starting point and ultimately closes the loop, because every test, every decision, and every adjustment exists to answer one question: Does this system produce profitable growth?

Related Insight

Response rates alone cannot determine how much capital a company should deploy for customer acquisition. Strategic growth decisions ultimately depend on the allowable Cost-Per-Sale, which defines the economic boundary for profitable expansion.

Explore that question in “How Much Should We Spend, in Total, to Acquire Customers This Year?”